This case study is illustrative and anonymized. It describes the kind of outcome model-versus-market edge detection is designed to produce. It is not a claim about a named client.

The problem

A betting syndicate had good instincts but no consistent way to measure them. Results swung match to match, and the team could not tell skill from variance.

The approach

The syndicate logged the price taken and the closing price for every position, and used model-versus-market edges to decide which prices to take. The model gave an independent probability, and the team acted only when the gap was large enough to matter.

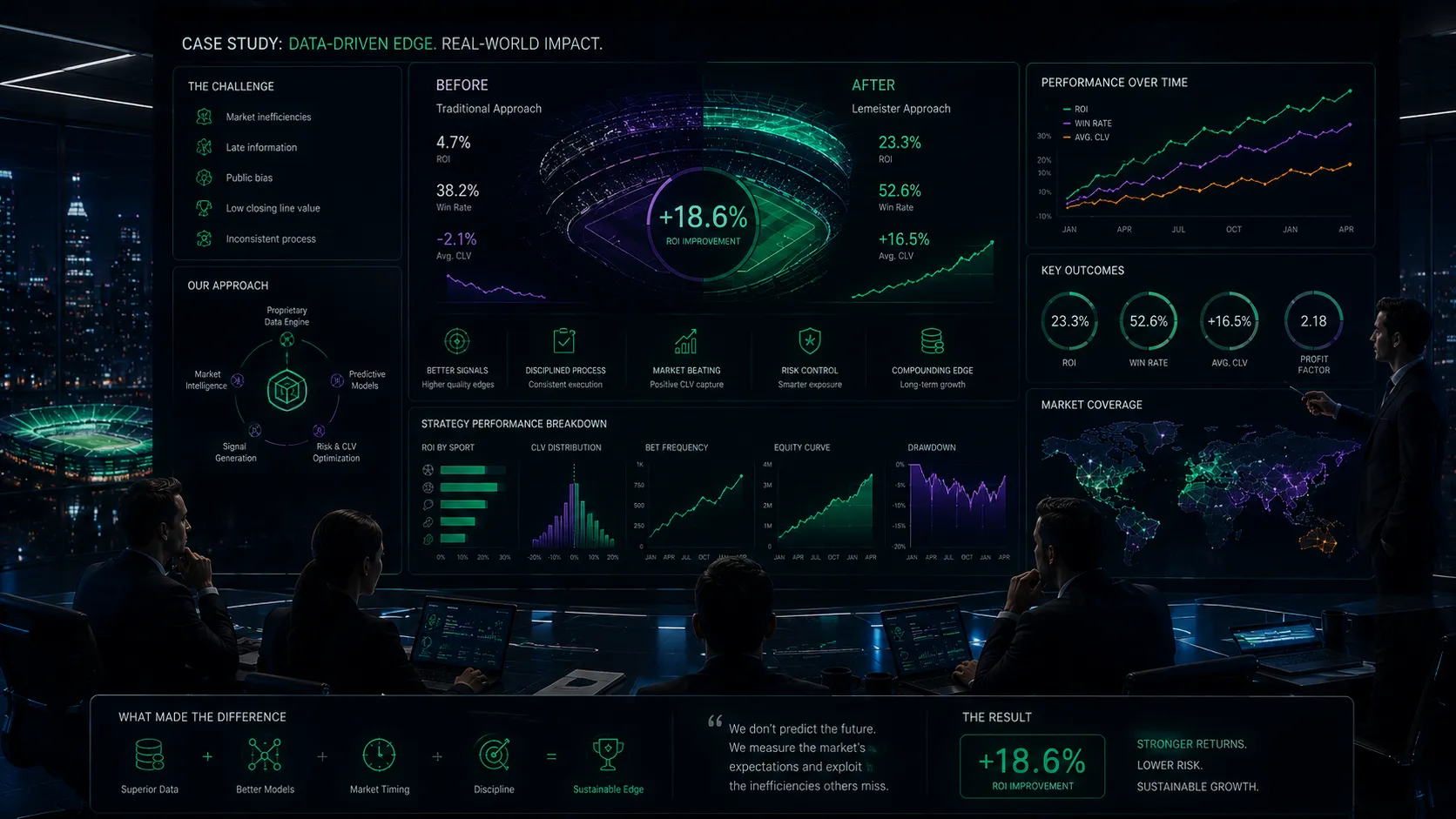

The illustrative outcome

In this scenario average closing line value turns reliably positive. The team stops judging itself on weekly profit and starts judging itself on whether it beat the close. Confidence through losing runs improves because the benchmark is sound.

The point

Edge detection is not a crystal ball. It is a discipline. The syndicate wins not by predicting results but by consistently taking better prices than the market closes at.

See closing line value and Desk pricing for the tier this illustrates.